Consumer Confidence: Labor Strength Meets the Inflation Squeeze

- Lingxiao Xu

- Apr 29

- 4 min read

Updated: 9 hours ago

The April confidence data look better on the surface than they do in the intertemporal budget constraint. The headline index edged higher, helped by a still-firm assessment of current labor-market conditions, but the same dashboard also shows the mechanism by which confidence can become fragile: inflation expectations, gasoline, shelter, and slowing real wage momentum are beginning to tax disposable income.

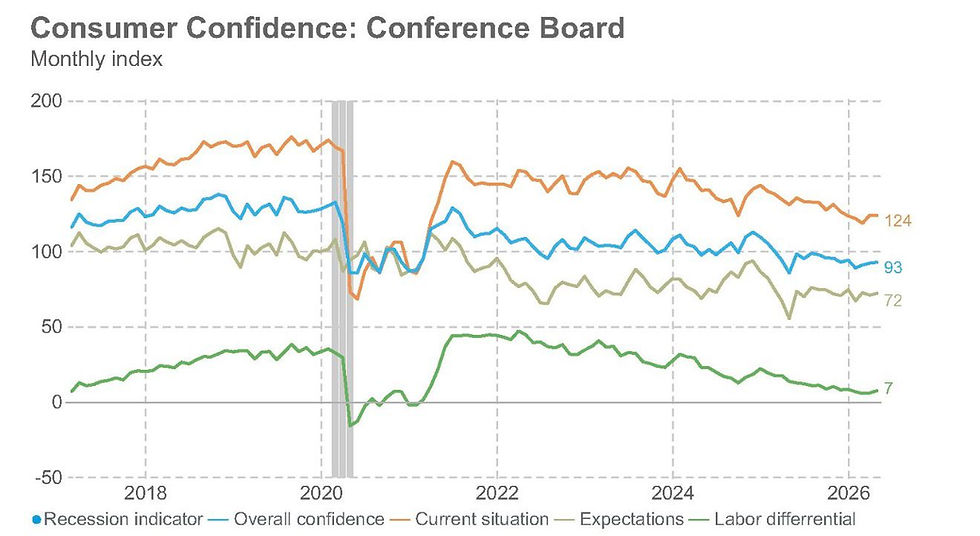

A Resilient Present Is Not the Same as a Durable Consumer Cycle

The chart’s most important separation is between the Present Situation measure and Expectations. Current conditions remain visibly stronger than the forward-looking component: the former sits near the 120s while expectations are closer to the low 70s, with the labor differential no longer showing the 2021–2022 excess-tightness impulse. That gap matters because consumption is not a simple function of today’s paycheck; it is a function of perceived permanent income, precautionary saving motives, and the price of liquidity.

In a permanent-income/lifecycle framing, households spend against the present value of expected labor income, not merely against last month’s payroll print. A compact way to write the channel is:

`C_t = α W_t + β E_t[PV(Y^L)] - γ σ_t + ε_t`

where consumption rises with wealth and expected labor income, but falls when income uncertainty or inflation uncertainty increases. April’s data are consistent with a positive `E_t[PV(Y^L)]` from employment, while `σ_t` is rising because price expectations and essential-cost volatility have moved against households.

The Data Map: Why the Same Report Contains Both Strength and Strain

Channel | Current signal | Consumption implication |

Headline confidence | about 102 versus about 101 expected | modest upside surprise |

Present Situation Index | about 146 in the source data; chart current-situation line still elevated | labor income remains the anchor |

Initial jobless claims | roughly 210–220k | layoffs are not yet the stress channel |

Payroll growth | roughly 175–200k per month | supports aggregate wage income |

1-year inflation breakevens | roughly 3.3–3.5% | raises expected cost of living |

Gasoline and shelter | gasoline up 15–20% YoY; shelter near 5–6% | compresses discretionary cash flow |

Retail control group | about 0.3–0.4% monthly growth | early moderation, not collapse |

This table is the thesis in miniature. Employment variables still look expansionary, but the inflation variables are increasingly regressive: gasoline and shelter absorb cash before consumers decide how much to spend on cyclical goods. A household can report that jobs are available and still reduce discretionary spending if its rent, commute, and insurance bills are repricing faster than wages.

Real Wages Are the Transmission Belt

The critical variable is not nominal wage growth near 4.0–4.3% year over year; it is real disposable wage growth after essential prices. If nominal wages rise 4.2%, but the experienced inflation basket for a renter who drives to work rises 5.5%, the household’s effective real wage change is approximately `4.2% - 5.5% = -1.3%`. That arithmetic is crude, but it captures why confidence can hold up briefly even as consumption breadth narrows.

This is where labor resilience and inflation pressure stop being independent stories. Tight labor markets support income, yet the same tightness can delay the disinflation in services and shelter-sensitive categories. The consumer, therefore, faces a mixed equilibrium: employment reduces default risk, while persistent prices reduce free cash flow.

Expectations, Gasoline, and the Psychology of Liquidity

Gasoline has an outsized behavioral effect because it is frequent, salient, and difficult to substitute in the short run. In New Keynesian terms, it is a relative-price shock that can contaminate inflation expectations; in household finance terms, it is a weekly liquidity drain. A 15–20% gasoline increase is not large enough by itself to determine national consumption, but it is highly visible enough to change the precautionary-saving rule for lower- and middle-income cohorts.

Shelter works more slowly but with greater persistence. Sticky shelter inflation near 5–6% means the largest household liability reprices with a lag, extending the squeeze even after headline CPI cools. That is why the forward inflation impulse matters more than the headline confidence uptick: once expected necessary spending rises, households lower the marginal propensity to consume out of incremental income.

Market Implication: Watch the Gap, Not Just the Level

For investors, the clean signal is the gap between present labor confidence and forward purchasing power. If labor data remain firm while inflation expectations drift higher, nominal revenue can look resilient for a while, but margin mix and volume quality deteriorate underneath. Staples, fuel, and shelter-linked outlays take share; discretionary categories depend increasingly on promotions, credit, and higher-income consumers.

The retail control group’s 0.3–0.4% monthly pace is therefore more informative than the confidence headline. It says demand is still growing, but the growth is losing convexity. In factor language, the consumer beta to labor income remains positive, while the consumer beta to inflation surprise has become more negative.

Conclusion: Confidence Is Anchored by Jobs, but Vulnerable to Prices

The material argument is not that the consumer is already breaking. It is that April’s modest confidence improvement rests on a labor-market foundation that is still solid—low claims, unemployment near 4%, and payroll gains around 175–200k—but that foundation is being tested by a forward inflation impulse. Higher breakevens, gasoline up 15–20%, sticky shelter inflation, compressed real wage growth, and slower control-group retail sales all point to the same conclusion: labor resilience is anchoring confidence today, yet erosion in real purchasing power is likely to challenge the sustainability of consumer strength over the coming quarters.

Comments