Inflation Swaps Signal Policy Patience, Not Victory

- Lingxiao Xu

- Jun 12

- 16 min read

Inflation Swaps Are Saying Central Banks Have Time, Not That Inflation Risk Is Gone

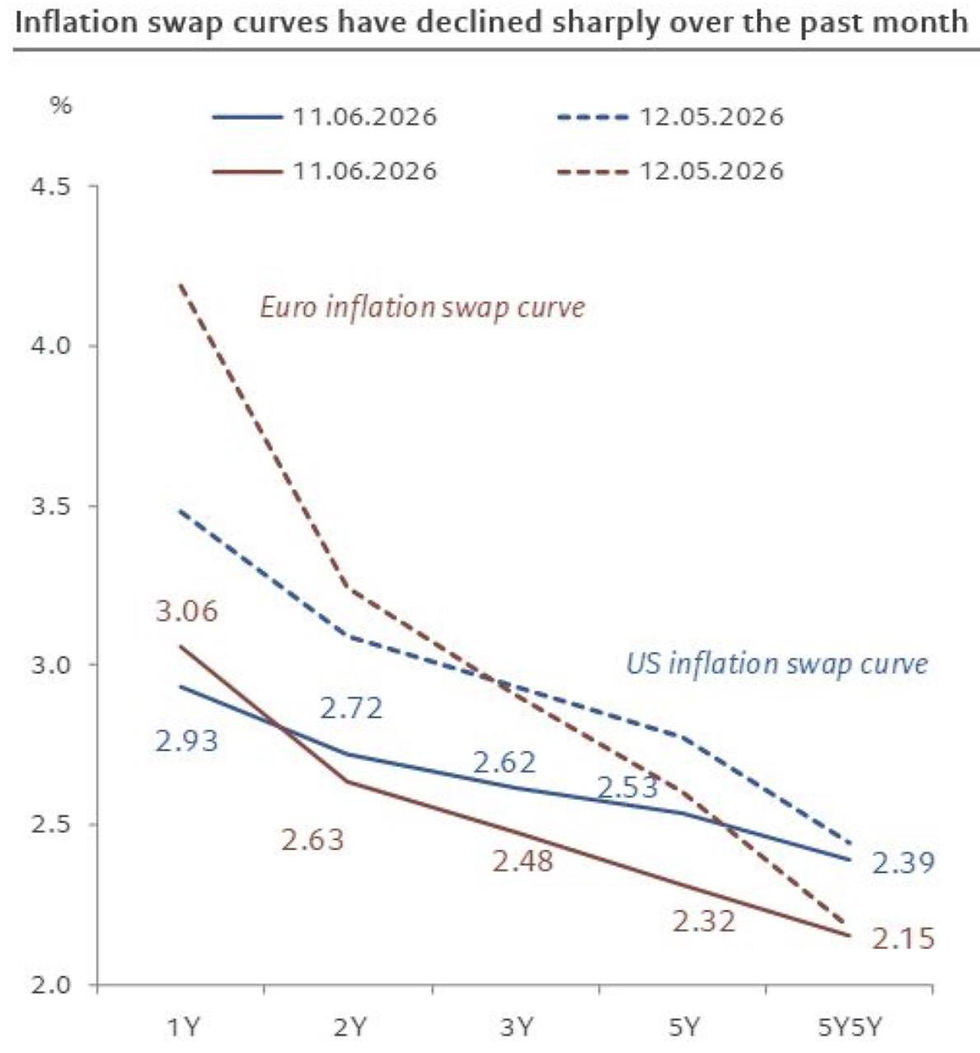

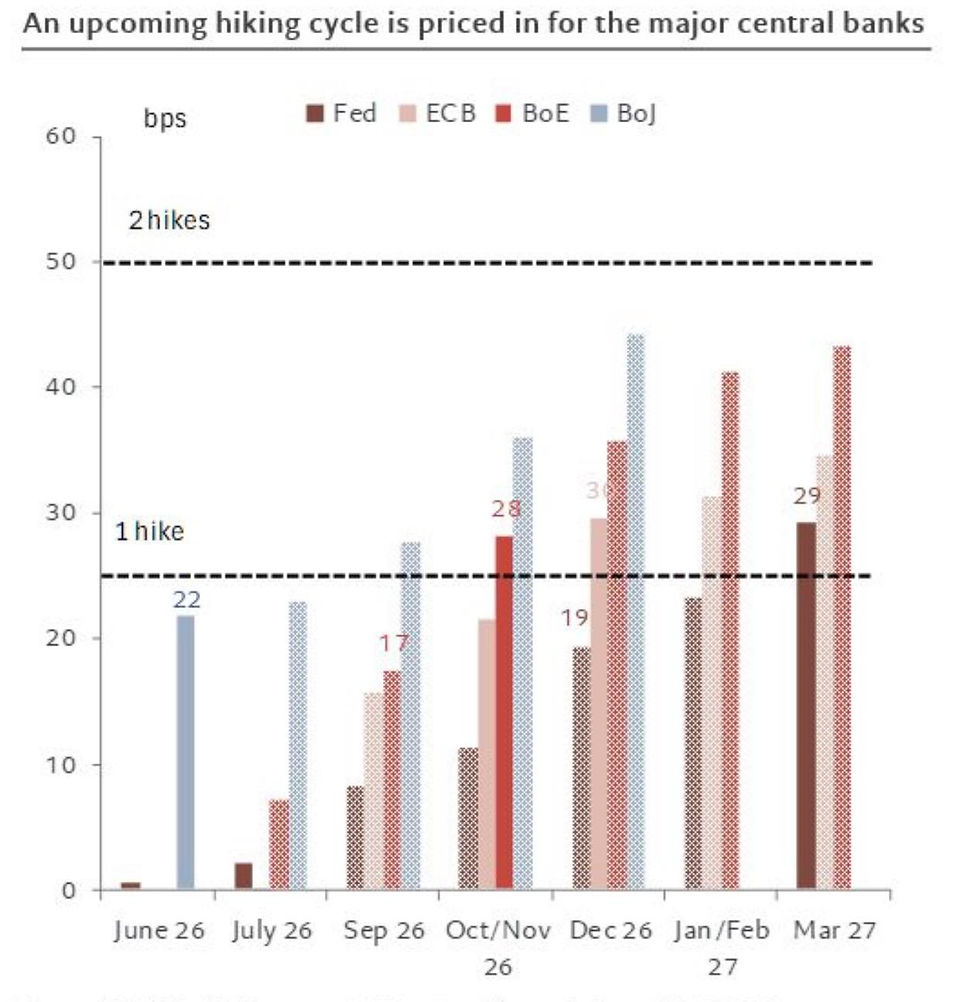

The sharp repricing in inflation swaps is important because it changes the market conversation from “central banks may need to react to every inflation wobble” to “central banks may have enough time to distinguish noise from persistence.” Eurozone one-year inflation swaps have fallen from above 4.2% to roughly 3.1%, while U.S. one-year inflation swaps have moved from about 3.5% to 2.9%. The move is not limited to the very front end. Five-year inflation swaps have declined to roughly 2.5% in the United States and 2.3% in Europe, and medium- and long-term inflation pricing has also moved lower. At the same time, markets no longer fully price a Federal Reserve rate hike in 2026. By March 2027, futures imply about one hike from the Fed, one from the European Central Bank, and almost two hikes each from the Bank of England and the Bank of Japan.

That configuration is not a declaration that inflation has disappeared. It is a statement about probability, sequencing, and policy patience. Inflation swaps are market prices for inflation compensation. They include expected inflation, inflation risk premia, liquidity, positioning, and the price of hedging. When they fall across the curve, the market is not merely marking down next month’s CPI. It is marking down the compensation required to own inflation risk over several horizons. That is a stronger signal than a single data release, but it is still a market signal rather than a physical law. It should be interpreted as a repricing of the inflation distribution, not as a guarantee that inflation will glide back to target without interruption.

Lower oil prices are the obvious driver, and they matter. Energy is the fastest-moving component in headline inflation expectations, the most visible price for households, and a key input for transportation, industrial production, chemicals, aviation, and utilities. When oil falls, headline inflation risk declines, near-term inflation swaps compress, and central banks gain room to avoid overreacting to temporary upside surprises. But the deeper question is whether lower oil is merely lowering headline inflation or also improving the medium-term inflation regime. The answer depends on whether energy relief reduces wage pressure, pricing behavior, inflation expectations, and corporate cost pass-through, or whether it simply masks still-sticky services inflation.

The disciplined reading is therefore balanced. The market is telling us that central banks have more time than they appeared to have when front-end inflation pricing was higher. It is not telling us that every inflation problem has been solved. In fact, the difference between the Fed, ECB, BoE, and BoJ pricing shows that the market is becoming more selective. It is not pricing one global inflation cycle. It is pricing different inflation regimes, different labor markets, different policy reaction functions, and different sensitivities to oil.

What Inflation Swaps Actually Measure

Inflation swaps are often discussed as if they were clean forecasts, but they are better understood as tradable inflation compensation. In a zero-coupon inflation swap, one side pays a fixed inflation rate and receives realized inflation over the life of the contract, or vice versa. The fixed rate is the market-clearing inflation swap rate. If the one-year inflation swap is 2.9%, the market is effectively setting a price at which investors can exchange fixed inflation compensation for realized inflation exposure over the next year. That rate reflects expected realized inflation, but it also reflects risk premia, balance-sheet costs, liquidity, collateral, hedging demand, and dealer intermediation.

This distinction matters because inflation swaps can fall for more than one reason. Expected inflation may decline. The inflation risk premium may decline. The demand for inflation hedges may ease. Energy traders, macro funds, pensions, insurers, and relative-value accounts may reduce inflation-linked exposures. Central-bank credibility may improve. Or lower oil may mechanically reduce the probability of high headline prints, making inflation protection less urgent. A falling swap rate is therefore not one single message. It is the aggregate price of many agents becoming less willing to pay for inflation insurance.

The curve shape is especially informative. A front-end decline can be mostly oil, base effects, and near-term CPI arithmetic. A decline across five-year and longer horizons says something more persistent. It suggests investors are reducing the probability that a temporary inflation shock becomes embedded in expectations and policy. That is why the move in five-year inflation swaps toward roughly 2.5% in the U.S. and 2.3% in Europe is important. It indicates that the market is not only marking down the next few prints; it is also reducing medium-term inflation compensation.

Still, the market is not pricing perfect normalization. A U.S. five-year inflation swap around 2.5% is not the same as a world in which inflation risk has returned to the pre-pandemic low-volatility regime. It remains above a strict 2% target, partly because inflation swaps refer to inflation indices and contain premia, and partly because investors still demand compensation for upside risk. Europe at roughly 2.3% looks closer to target, but even there, the level does not imply no risk. It implies that the market has moved from acute inflation fear toward moderated inflation risk.

Why Oil Is Powerful, but Not Sufficient

Oil is powerful because it operates through both arithmetic and psychology. The arithmetic is straightforward: lower crude prices reduce gasoline, diesel, jet fuel, petrochemical inputs, and transportation costs with varying lags. The direct weight of energy in consumer price indices is smaller than the emotional weight households place on gasoline, but it is still large enough to matter for headline inflation. Lower oil also reduces costs for firms that depend on freight, distribution, and energy-intensive production. That helps compress near-term inflation swaps.

The psychological channel is just as important. Households and firms do not observe the entire price system every day. They observe highly salient prices: gasoline, groceries, rent, utilities, insurance, and mortgage rates. Oil prices influence one of the most visible daily prices. When energy falls, inflation expectations can become less anxious, even if services prices are still sticky. That matters because inflation expectations affect wage bargaining, corporate pricing behavior, and central-bank communication.

The policy channel follows from those two effects. If oil is falling, central banks can be less reactive to one or two firm inflation prints. They can argue that headline volatility is being dampened by energy, that expectations are better behaved, and that policy should focus on the persistence of core inflation and wages rather than every short-run movement. This is the core of the current market repricing: lower oil gives central banks a reason to remain patient.

But oil is not sufficient because the inflation process is broader than energy. Services inflation, wages, rents, insurance, healthcare, taxes, regulated prices, and supply-chain margins can keep inflation elevated even when energy falls. A lower oil price can buy time without solving the underlying problem. The market’s mistake in some past cycles has been to treat energy disinflation as equivalent to structural disinflation. The correct approach is to ask whether energy relief is being reinforced by lower wage growth, lower services inflation, softer demand, and lower pricing power. If those confirmations do not arrive, inflation swaps can reprice upward again.

The U.S. Signal: Less Need for a 2026 Fed Hike

The U.S. part of the repricing is especially important because markets no longer fully price a Fed hike in 2026. This is a meaningful shift in the reaction-function narrative. A fully priced hike would imply that the market believed inflation persistence or growth resilience would force the Fed back into tightening. The current pricing says that the bar for renewed tightening has risen. The Fed may still keep policy restrictive for longer, but the market is less convinced that it must restart the hiking cycle.

By March 2027, futures imply roughly one Fed hike, or about 29 basis points. That is not aggressive. It is a small amount of tightening priced over a relatively long horizon, and it can be read as a hedge against inflation persistence rather than a base case of renewed inflation crisis. The market is saying that the Fed may need to lean against inflation again if disinflation stalls, but it is no longer treating that outcome as immediate or unavoidable.

This fits the decline in U.S. one-year inflation swaps from roughly 3.5% to 2.9%. The front end is still above target-consistent levels, but the direction is helpful. It implies that the market sees less near-term headline pressure, likely helped by energy. The five-year swap around 2.5% says medium-term inflation compensation remains above the Fed’s preferred comfort zone, but not high enough to demand an urgent hawkish repricing. In other words, the Fed has time.

The risk is that time can be misused. If financial conditions ease too much, demand may remain firm and services inflation may not cool. If oil rebounds, the front-end relief can disappear quickly. If wages remain sticky, the five-year part of the curve can reprice. The market’s current message is not “cut without concern” or “inflation is over.” It is “do not overreact to near-term volatility while the inflation compensation curve is moving lower.” That is a subtle but important difference.

The Eurozone Signal: More Disinflation, More Fragility

The Eurozone one-year inflation swap decline from above 4.2% to about 3.1% is larger than the U.S. decline in level terms. Europe has been more visibly exposed to energy shocks, imported inflation, and the after-effects of the earlier gas crisis. When energy prices fall and supply risks moderate, Europe’s inflation market can reprice faster. The fall in medium-term expectations, with five-year swaps around 2.3%, also suggests that the market is becoming more confident that the ECB can avoid another inflation surge.

But Europe’s lower inflation compensation must be interpreted alongside weaker growth sensitivity. The Eurozone can get disinflation through a healthier supply picture, but it can also get disinflation through weaker demand. Those are different investment regimes. If inflation swaps are falling because energy pressure is easing while real incomes stabilize, that is constructive. If they are falling because growth is fragile and demand is softening, the signal is less bullish for risk assets.

The ECB pricing by March 2027 implies about one hike, or roughly 35 basis points. That is slightly more than the Fed in basis-point terms, but still not a dramatic tightening path. It suggests the market sees the ECB as able to remain patient, while retaining some probability that inflation persistence could require a policy response. The difference from the U.S. is that Europe’s inflation shock has had a larger imported-energy component, while U.S. inflation has been more tied to domestic demand, housing, wages, and services.

This means Europe’s inflation repricing is more vulnerable to external shocks. A rebound in oil or gas, geopolitical disruption, or currency weakness can alter the picture quickly. At the same time, weaker growth can cap the pass-through of those shocks. The market is balancing those forces. The current swap levels say the acute inflation scare has cooled, but they do not say the European inflation regime is permanently back to its pre-2020 state.

Why the BoE and BoJ Are Priced Differently

The Bank of England and Bank of Japan stand out because futures imply nearly two hikes each by March 2027, around 43 basis points for the BoE and 44 basis points for the BoJ. This is not a random detail. It shows that markets are not simply applying a global lower-inflation narrative to every central bank. They are distinguishing between jurisdictions where inflation relief creates patience and jurisdictions where the policy path may still require normalization.

For the Bank of England, the issue is persistent domestic inflation pressure. The U.K. has faced a difficult mix of wage growth, services inflation, labor-market frictions, and imported price shocks. Even when energy helps, the inflation process can remain sticky because services and wages are slow-moving. The market’s pricing of almost two hikes by 2027 can be read as a belief that the BoE may have less room to relax than the Fed or ECB. It may need to maintain or reassert restrictive policy if domestic inflation does not cool enough.

For the Bank of Japan, the logic is different. Japan is not priced for hikes because it has the same inflation problem as the U.K. It is priced for hikes because the policy normalization path is still incomplete. After years of ultra-low rates, yield-curve control, and low inflation expectations, Japan’s inflation and wage dynamics have changed enough for markets to price gradual normalization. A BoJ hike is less a sign of inflation panic and more a sign that Japan may be exiting an exceptional monetary regime.

This distinction matters for cross-asset investing. A Fed hike priced in 2027 would likely signal inflation persistence or excessive demand. A BoJ hike could signal normalization and yen support. A BoE hike could signal sticky wage-services inflation and pressure on rate-sensitive U.K. assets. The same number of basis points can mean different things because central-bank reaction functions are different.

The Cross-Market Message: Inflation Risk Is Becoming More Local

The broad decline in inflation swaps might look like a single global story, but the policy pricing reveals a more local picture. U.S. and European inflation compensation is falling, helped by lower oil and a reduction in near-term inflation anxiety. Yet the expected policy paths differ across the Fed, ECB, BoE, and BoJ. That tells us the global inflation shock is no longer being priced as one synchronized event. Markets are moving toward a more differentiated regime.

This is important because the post-pandemic inflation cycle initially had a strong global component. Supply-chain disruption, fiscal demand, energy shocks, and goods shortages affected many economies at once. Central banks tightened in broadly overlapping windows. Correlations across rates markets rose. But as the shock matures, local differences matter more: wage bargaining institutions, mortgage structures, energy dependence, fiscal policy, currency pass-through, demographics, productivity, and central-bank credibility.

In that world, a simple “long global duration because inflation is falling” trade may be too blunt. The better trade construction is relative. Which inflation markets have overreacted to oil? Which central banks have the most patience? Which economies still have sticky services inflation? Which currencies benefit from policy normalization? Which yield curves embed too much or too little future tightening? The current data encourage relative-value thinking rather than a single global macro slogan.

The same applies to equities and credit. Lower inflation swaps can support risk appetite by reducing discount-rate pressure and tail risk. But if disinflation comes from weak demand, cyclicals may not benefit. If oil falls, consumers may gain real income, but energy producers and commodity-linked credit may suffer. If central banks remain patient, duration-sensitive equities may benefit, but only if earnings are not deteriorating. The cross-market signal is supportive, but not universally bullish.

Portfolio Implications: Duration, Breakevens, Equities, and Currency

For duration, the decline in inflation swaps reduces the urgency of hawkish repricing. That should support government bonds, especially where markets had over-priced the risk of renewed tightening. However, the support is conditional. If real yields fall because inflation risk falls while growth remains stable, duration can rally alongside equities. If nominal yields fall because growth fears rise, the equity interpretation is different. Investors should separate the inflation component from the growth component.

For inflation-linked assets, the signal is more nuanced. Lower inflation swaps make inflation protection cheaper than it was when the front end was stressed. But they also reflect less immediate need for hedging. The decision depends on whether an investor believes lower oil has genuinely changed the medium-term inflation distribution. If the answer is yes, reducing inflation hedges makes sense. If the answer is no, the decline in swaps may create a better entry point for selective inflation protection, especially in portfolios exposed to wage, rent, energy, or commodity shocks.

For equities, the most direct benefit is lower discount-rate uncertainty. Growth equities, long-duration cash flows, and rate-sensitive sectors tend to benefit when inflation compensation falls and central banks appear less likely to tighten. But the equity signal is strongest when lower inflation is not caused by collapsing demand. If oil-driven disinflation supports real incomes and leaves earnings intact, the outcome is constructive. If falling inflation swaps reflect weakening nominal growth, earnings risk can dominate valuation relief.

For currencies, relative policy pricing matters. A market that prices less Fed tightening but more BoJ normalization can support yen strength, depending on risk sentiment. A BoE path that remains more hawkish can support sterling in rate terms, but only if growth and external balances do not deteriorate. The euro’s response depends on whether lower inflation pricing is seen as ECB credibility, energy relief, or weak demand. Currency markets will not trade inflation swaps in isolation; they will trade the interaction of inflation, growth, and policy.

Scenario Map

The first scenario is benign disinflation. Oil remains lower, goods and energy relief flow through headline inflation, wage growth cools gradually, services inflation decelerates, and central banks stay patient. Inflation swaps continue to drift lower or stabilize near target-consistent levels. This is supportive for duration, quality equities, credit spreads, and a soft-landing narrative.

The second scenario is temporary oil relief. Inflation swaps fall because energy falls, but services and wages remain sticky. Central banks do not hike immediately, but they also cannot validate aggressive easing. Inflation swaps stop falling and eventually reprice higher if oil rebounds or core inflation stalls. This scenario favors patience, curve optionality, and selective inflation hedges rather than outright disinflation positioning.

The third scenario is growth-led disinflation. Inflation swaps fall because demand is weakening, not only because oil is lower. Central banks gain room to avoid hikes, but earnings expectations decline and credit risk rises. Duration can perform, but equities may struggle. This is the classic case where lower inflation pricing is not automatically good news for risk assets.

The fourth scenario is policy divergence. The Fed and ECB remain patient, the BoE stays constrained by sticky domestic inflation, and the BoJ continues gradual normalization. Cross-market rates and currency relative value become more important than outright inflation direction. This is the scenario most consistent with the current pricing details: lower global inflation compensation, but differentiated expected hikes by central bank.

A Practical Reading of the Numbers

The actual levels help clarify the market message. A Eurozone one-year inflation swap near 3.1% is still not low in an absolute sense, especially relative to a 2% inflation objective. But the fall from above 4.2% is large enough to reduce the perceived need for an urgent policy response. It says that the market has moved from pricing a potentially disorderly near-term inflation profile to pricing a still-elevated but less dangerous one. That is a major distinction for central-bank communication. A central bank can tolerate an elevated one-year inflation price if the direction is falling and medium-term compensation is anchored. It has a harder time doing so when the front end is rising and the five-year point is also drifting higher.

The U.S. one-year swap near 2.9% sends a similar message. It remains above target-consistent comfort, but it is far less alarming than a front end moving higher while the labor market is tight and oil is rising. The five-year U.S. inflation swap near 2.5% is the more important anchor. It says investors still price some inflation premium, but not enough to force the Fed into a new tightening narrative by itself. The difference between 2.9% at one year and 2.5% at five years also implies that the market sees near-term inflation risk as higher than medium-term inflation risk. That is exactly the shape policymakers prefer if they want to look through transitory volatility.

Europe’s five-year level near 2.3% is closer to a credible normalization story. The reason the ECB still has to be cautious is that Europe’s inflation basket has been highly sensitive to energy and currency shocks. A lower swap level can coexist with vulnerability to a new external impulse. This is why the move should not be read as unconditional dovishness. It is conditional patience: patience as long as energy stays contained, wage growth does not reaccelerate, and inflation expectations remain stable.

The futures pricing reinforces the same idea. Roughly 29 basis points of Fed tightening by March 2027 is close to one hike, but it is not a forceful tightening cycle. Roughly 35 basis points for the ECB is also modest. The BoE and BoJ near 43 to 44 basis points are more meaningful because they point to a different local story. The market is saying that the Fed and ECB are closer to wait-and-see mode, while the BoE may still be constrained by domestic inflation persistence and the BoJ may still be moving along a normalization path.

For a portfolio manager, the difference between these numbers changes implementation. If the thesis is simply that inflation risk is falling globally, one might buy duration everywhere. If the thesis is that oil has reduced the near-term inflation tail while central-bank paths remain differentiated, the better implementation may be long duration where inflation risk premia remain too high, relative-value curve trades where future hikes are mispriced, and currency expressions that capture the difference between Fed patience and BoJ normalization. The same macro observation can lead to very different positions depending on whether the investor treats it as a level signal, a curve signal, or a relative policy signal.

The numbers also matter for risk management. A move from 4.2% to 3.1% in Eurozone one-year swaps is already a large repricing. Chasing the move after it has happened requires confidence that oil remains lower and that core inflation confirms the signal. If the confirmation fails, the front end can retrace quickly. Conversely, if the five-year point continues to decline while policy-hike pricing fades, the market will increasingly treat this as a genuine disinflation regime. The next phase therefore depends less on the first move and more on confirmation from wages, services inflation, realized energy prices, and central-bank language.

Research Anchors for the Repricing

Several bodies of research help frame this move. The first is the expectations-augmented Phillips curve tradition, which says inflation depends not only on slack but also on expected inflation and supply shocks. Lower oil reduces the supply-shock component and can help expectations, but it does not automatically eliminate wage or services pressure. That is why central banks can be patient without becoming complacent.

The second is term-structure research. Inflation swap curves embed expectations and risk premia over different horizons. A front-end move can be dominated by energy and base effects; a five-year move reflects broader beliefs about inflation persistence, credibility, and hedging demand. When both front-end and medium-term swaps fall, the market is reducing both near-term inflation fear and medium-term inflation compensation.

The third is risk-premium research in macro-finance. Investors require compensation for states of the world in which inflation is high when growth is weak or central banks are forced to tighten into fragility. If lower oil reduces the probability of those bad states, inflation risk premia can fall. That can lower nominal yields even if expected real growth is not changing much.

The fourth is international monetary economics. Central banks face different inflation processes because economies differ in openness, wage-setting, energy dependence, exchange-rate pass-through, and financial structure. A synchronized oil move can lower inflation pricing everywhere, but policy pricing can still diverge. That is exactly what the market is showing through the different implied paths for the Fed, ECB, BoE, and BoJ.

Conclusion: Patience Is the Message, Not Victory

The current inflation-swap repricing is a meaningful improvement in the inflation outlook. Eurozone one-year swaps moving from above 4.2% to around 3.1%, U.S. one-year swaps moving from about 3.5% to 2.9%, and five-year swaps falling toward roughly 2.5% in the U.S. and 2.3% in Europe all point in the same direction: markets are demanding less compensation for inflation risk. Lower oil is a key driver, and it gives central banks room to avoid overreacting to short-term volatility.

But the correct conclusion is not that inflation risk is gone. The correct conclusion is that the market has shifted from acute inflation fear to policy patience. Central banks can watch the data rather than pre-commit to renewed tightening. The Fed is no longer fully priced for a 2026 hike. The ECB has more room to wait. The BoE and BoJ remain priced for more tightening by 2027 because their domestic regimes and policy starting points differ.

For investors, this means the easy headline is less useful than the distribution. Lower inflation swaps support duration and can help risk assets, but only if disinflation is benign rather than growth-led. Lower oil helps, but only if it also reduces expectations, wages, and services pressure. Policy divergence matters, because the same inflation shock does not mean the same thing in the U.S., Europe, the U.K., and Japan. The market’s message is constructive, but conditional: central banks have more time, inflation risk is less acute, and the next phase will be decided by whether lower energy prices become broader disinflation or merely a temporary relief valve.

Comments