Tight Credit Spreads Are Hiding a More Uneven Default Cycle

- Lingxiao Xu

- May 11

- 5 min read

Updated: 9 hours ago

Tight Credit Spreads Are Hiding a More Uneven Default Cycle

Headline credit markets look calm. U.S. high-yield spreads are near the tight end of historical ranges, around 270–280 basis points, while investment-grade spreads remain below roughly 80 basis points. Business Development Companies and private-credit-linked risk assets have also rebounded alongside broader markets. On the surface, credit investors appear to be underwriting a soft landing, resilient earnings, and ample refinancing access.

The problem is that the surface is not the structure. Beneath tight index spreads, syndicated loans remain materially wider, lower-rated single-B borrowers and high-yield technology credits still trade with meaningful risk premia, and speculative-grade default activity remains elevated around 4–5% rather than normalizing toward the long-term average near 3%. Distressed exchanges, liability-management exercises, and amend-and-extend transactions further blur the boundary between “no default” and “economic impairment.” The credit market is not broadly risk-on; it is selectively risk-on.

Two Charts, One Message

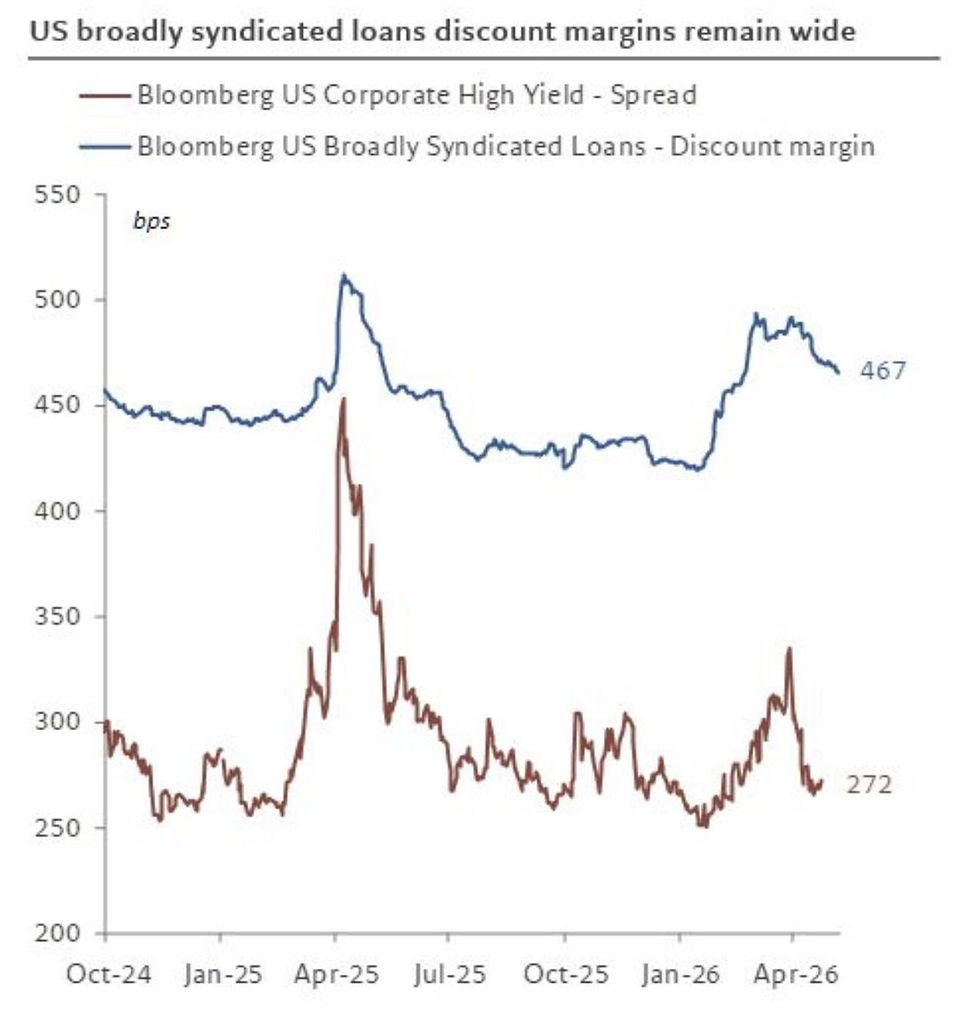

The first chart shows a sharp divergence between broadly syndicated loan discount margins and high-yield bond spreads. Loan discount margins remain near 467 basis points, while U.S. high-yield bond spreads are closer to 272 basis points. The gap is roughly 195 basis points. The second chart shows that the global default cycle has not improved as quickly as expected, especially in loans. Loan default rates surged toward the high-single-digit zone before easing, and baseline forecasts still point to defaults above the benign pre-tightening regime.

Indicator | Current signal | Why it matters |

U.S. high-yield spread | ~272 bps | Broad bond index prices a benign macro outcome |

U.S. loan discount margin | ~467 bps | Floating-rate, lower-quality borrowers require more compensation |

Loan-HY spread gap | ~195 bps | Credit risk is dispersed, not uniformly tight |

Speculative-grade defaults | ~4–5% | Stress remains above long-run normal levels |

Long-run default average | ~3% | Normalization has been slower than hoped |

The central inference is simple: index-level spread compression is real, but it is not comprehensive. The credit cycle has narrowed at the top while remaining messy underneath.

Why Loans Are Telling a Different Story

Loans and bonds are not interchangeable credit instruments. Broadly syndicated loans are typically floating-rate, secured, and senior, but the borrower universe often includes highly levered companies that are directly exposed to higher short-term rates. High-yield bonds have more fixed-rate duration and often reflect a somewhat different issuer mix. A loan can therefore offer a wider discount margin not because it is obviously cheap, but because its borrowers are living with higher cash interest expense today.

A simple interest-coverage example is useful. Suppose a leveraged borrower has $100 of debt and $12 of EBITDA. At a 5% cash interest rate, interest expense is $5 and coverage is `12 / 5 = 2.4x`. At a 9% cash interest rate, interest expense is $9 and coverage falls to `12 / 9 = 1.3x`. The company may still avoid a formal default, but its equity cushion, reinvestment capacity, and refinancing flexibility have all been impaired.

That is why loans can remain wide even when high-yield spreads compress. Floating-rate structures transmit monetary tightening directly into borrower cash flows.

The Default Cycle Is Being Managed, Not Eliminated

The persistence of 4–5% speculative-grade default activity matters because spreads usually compensate investors for expected loss, liquidity risk, and risk aversion. Expected credit loss can be approximated as:

`Expected loss ≈ default probability × (1 - recovery rate)`.

If defaults are 5% and recovery is 40%, expected annual credit loss is `5% × 60% = 3.0%`. A 272 bps high-yield spread offers less than that before accounting for liquidity, downgrade risk, volatility, taxes, and manager fees. The comparison is intentionally rough, because index spreads and realized defaults do not map one-for-one. But it shows why tight spreads are less comfortable when defaults remain elevated.

The complication is that modern credit cycles increasingly use liability-management techniques to delay formal recognition. Distressed exchanges, uptier transactions, drop-down financings, amend-and-extend deals, and covenant renegotiations can prevent immediate bankruptcy while still transferring value away from existing creditors. In Minsky terms, the system may be stabilizing cash flows by extending the balance-sheet fragility rather than removing it.

Dispersion Is the Real Regime

The important signal is not “credit is cheap” or “credit is expensive.” It is dispersion. Higher-quality public credit indices can look extremely tight while weaker loan borrowers, single-B issuers, and technology-related high-yield credits remain 150–300 basis points wider than broad averages. That is consistent with a market willing to own carry, but unwilling to ignore idiosyncratic refinancing risk.

Segment | Market behavior | Interpretation |

Investment grade | Very tight spreads | Balance sheets still trusted; demand for quality carry remains strong |

Broad high yield | Tight headline spreads | Soft-landing pricing dominates index level |

Syndicated loans | Discount margins still wide | Borrower-level stress and liquidity premium persist |

Single-B / stressed sectors | Wider risk premia | Market is discriminating by refinancing vulnerability |

Private credit / BDCs | Rebounded with risk assets | Marking lag and yield demand can coexist with latent stress |

This is a classic late-cycle pattern. The average looks stable because the highest-quality and most liquid instruments recover first. The tails remain fragile.

Energy and Macro Pressure Can Reprice the Tails

Credit is rarely hurt by one variable in isolation. The downside case is a combination: slower nominal growth, still-restrictive real rates, sector-specific energy or commodity pressure, and a refinancing calendar that forces weaker borrowers back to market before margins have recovered. Under that scenario, the gap between headline spreads and default activity becomes harder to defend.

The monetary-transmission channel is also lagged. Companies refinanced aggressively when rates were low, so the full effect of higher rates arrives only as maturities roll. Amend-and-extend transactions reduce near-term default risk, but they can also create a larger maturity wall later. The market may be buying time, not solving the underlying debt-service problem.

Investment Implications

For allocators, the charts argue against treating tight index spreads as a clean bill of health. Carry can still be attractive, particularly when all-in yields remain high, but the margin of safety is uneven. The better opportunity is not indiscriminate credit beta; it is security selection across capital structure, covenant quality, maturity schedule, and sector cash-flow resilience.

Loans may appear compelling because their discount margins are wider, yet the wider spread is compensation for real borrower stress. High-yield bonds may appear safer because spreads are tighter, yet tight spreads leave less room for error if defaults stay elevated. Private credit and BDC exposure may benefit from floating-rate income and less daily mark-to-market volatility, but those same features can obscure deterioration until restructurings occur.

Conclusion: The Market Is Selective, Not Complacency-Free

The core thesis is that headline credit resilience is genuine but incomplete. High-yield and investment-grade spreads imply confidence, while loans, single-B issuers, technology-related high-yield credits, and default data reveal a more fractured cycle. The continued use of distressed exchanges and maturity extensions suggests that some stress is being managed rather than cured. If growth slows, financial conditions tighten, or energy-related macro pressure persists, broad credit indices may need to reprice toward the risk already visible in the weaker segments. Tight spreads are not wrong by definition, but they leave little room for a default cycle that refuses to normalize.

Comments