Why the Entire Treasury Curve Is Under Upward Pressure

- Lingxiao Xu

- 5 days ago

- 10 min read

Updated: 7 hours ago

Why the Entire Treasury Curve Is Under Upward Pressure

The current U.S. Treasury curve is not being pushed higher by one simple story. It is being pulled upward by three different forces at once. The front end is reacting to inflation and the Federal Reserve's reaction function. The belly is absorbing a heavy mix of Treasury supply and corporate duration, especially from large technology companies financing AI and data-center investment. The long end is repricing the fiscal and term-premium problem: persistent deficits, large Treasury issuance, less central-bank balance-sheet support, and rising unease about long-run debt sustainability.

That distinction matters because a yield curve is not a single price. It is a strip of prices for different kinds of macro risk. A three-month bill is mostly a statement about expected policy over the next few meetings. A five-year note is a statement about the path of policy, the economy, and investor balance-sheet capacity over a medium horizon. A thirty-year bond is a statement about inflation credibility, fiscal trust, convexity demand, and the compensation investors require to hold duration through regimes they cannot fully forecast.

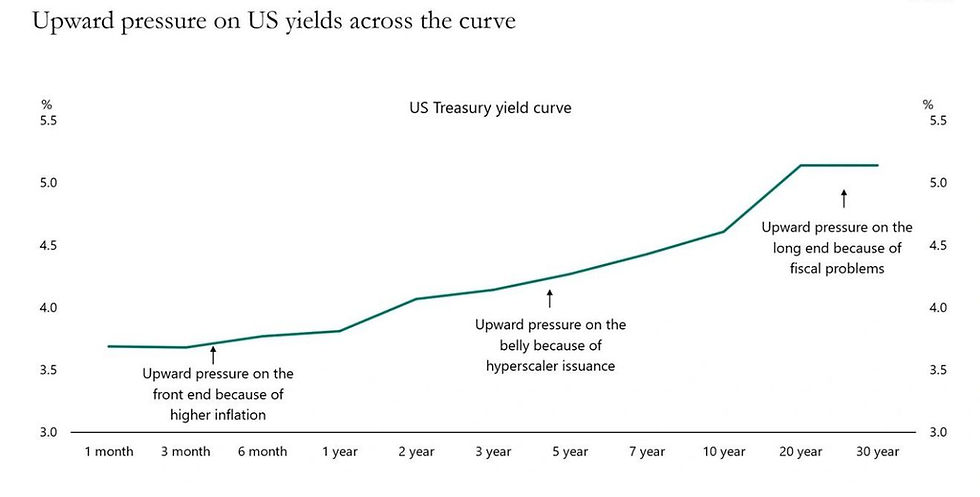

The chart's core message is therefore powerful: upward pressure is visible across the curve, but each segment is under pressure for a different reason. Treating the whole move as simply higher rates misses the more important point. The market is repricing the front end as an inflation problem, the belly as a supply-absorption problem, and the long end as a term-premium problem.

What the Curve Is Saying

The chart plots the U.S. Treasury yield curve from one month through thirty years. The line slopes higher from the bill sector toward the long bond, with three annotations. The front end is under upward pressure because inflation remains too high. The belly is under upward pressure because of hyperscaler issuance. The long end is under upward pressure because of fiscal problems.

This is a clean framework for understanding why a curve can steepen even when monetary policy is not necessarily becoming more restrictive at every horizon. The front end is anchored by the Federal Reserve's expected policy rate. If inflation runs above target, markets reduce the probability of aggressive rate cuts and demand a higher path for short-dated rates. The two-year and three-year sectors then inherit that higher-for-longer expectation.

The five-year to ten-year sector has a different problem. It is where macro expectations meet duration supply. Investors must absorb not only Treasury issuance but also a historic wave of corporate borrowing. Hyperscalers building AI infrastructure are issuing debt to fund data centers, chips, power procurement, networking, and cloud capacity. Even when those companies are creditworthy, their borrowing still adds duration to portfolios that already have to digest large sovereign supply.

The twenty-year and thirty-year points carry the deepest fiscal message. Long bonds require investors to accept uncertainty about inflation, issuance, fiscal policy, and future demand for safe assets. When deficits remain large and Treasury supply keeps expanding, investors demand more compensation. That compensation is the term premium.

Three Segments, Three Drivers

Curve segment | Main pressure | Transmission channel | Market implication |

Front end | Inflation above target | Fewer and slower expected Fed cuts | Policy-rate expectations stay elevated |

Belly | Treasury plus corporate duration supply | Investors must absorb more intermediate maturity paper | Five- to ten-year yields become more supply sensitive |

Long end | Fiscal deficits and term premium | Higher required compensation for long-duration risk | Curve steepening can persist even without a new growth boom |

The key is not that these drivers are independent. They interact. Sticky inflation raises the expected policy path, which raises funding costs. Higher funding costs make deficits more expensive, which worsens the fiscal arithmetic. Heavy Treasury supply competes with corporate issuance for investor balance-sheet space. If investors become saturated with duration, even high-quality borrowers need to pay more. A curve-wide move can therefore emerge from linked but distinct pressures.

Front End: Inflation and the Fed's Reaction Function

The front end of the curve is where monetary policy is most visible. A one-month bill, three-month bill, or one-year bill does not primarily trade on distant fiscal sustainability. It trades on where the policy rate is today and where investors think it will be over the next several meetings. When inflation remains above the Federal Reserve's target, the front end naturally resists falling.

In a simple expectations framework, a short Treasury yield can be approximated as:

`Short yield = expected average policy rate over the instrument's life + small risk and liquidity adjustments`

If investors previously expected the Fed to cut quickly, the front end can rally. But if inflation data remain firm, that expected path shifts upward. Suppose the market moves from expecting four 25-basis-point cuts over the next year to expecting only one. That is a 75-basis-point change in the expected policy path. Even before considering risk premia, the front end has a reason to reprice higher.

The mechanism is straightforward. Inflation above target makes the Fed reluctant to ease aggressively because easing too early risks validating the inflation impulse. The labor market can slow, but if core inflation or services inflation remains sticky, the Fed's credibility constraint dominates. In reaction-function language, the central bank is not optimizing only for near-term growth. It is also defending the long-run anchor for inflation expectations.

That is why the front end can remain elevated even when investors see signs of economic cooling. A softer economy is normally a rate-cut argument. But a softer economy with still-high inflation is not the same thing. The Fed can tolerate slower growth more easily than it can tolerate a renewed inflation psychology.

Belly: The AI Capital Cycle Meets Treasury Supply

The belly of the curve is more complicated because it sits between policy expectations and long-horizon risk premia. Five-year to ten-year yields reflect the expected path of short rates, but they also reflect how much duration investors must absorb. This is where the corporate borrowing surge becomes important.

The AI infrastructure buildout is capital intensive. Large technology companies need data centers, power, cooling, fiber, semiconductor supply agreements, and cloud infrastructure. These investments can be funded with internal cash flow, equity, partnerships, or debt. When the debt channel expands, the market receives more corporate bonds, often in maturities that compete directly with Treasury notes for investor duration budgets.

Even if the credit risk is low, duration is still duration. A high-quality corporate bond with a five- to ten-year maturity still exposes the buyer to interest-rate risk. Portfolio managers do not have infinite balance sheets. Insurance companies, pension funds, asset managers, banks, and foreign reserve managers all face limits on how much duration they want at a given yield. When both Treasury and corporate issuers are asking the market to absorb more paper, yields may need to rise until enough demand appears.

This is not just a credit-spread story. It is a duration-supply story. If a hyperscaler issues a large bond deal, the direct effect may be visible in corporate spreads and new-issue concessions. But the broader effect is that the market's aggregate duration supply has increased. Investors who buy the corporate bond may sell Treasuries, hedge with rates, or reduce purchases elsewhere. The adjustment can show up in Treasury yields even when the corporate issuer is viewed as safe.

A useful way to think about the belly is:

`Intermediate yield = expected policy path + inflation risk + duration supply premium + liquidity preference`

The first two terms are macro. The third term is market structure. In a world of heavy Treasury issuance and rising AI-related corporate borrowing, the duration supply premium becomes harder to ignore.

Why Hyperscaler Issuance Matters Beyond Tech

The word hyperscaler can make the issue sound narrow, but the macro implication is broad. AI investment is not just software spending. It is a physical capital cycle. Data centers require land, electricity, grid connections, cooling systems, chips, construction labor, and long-term power commitments. The financing needs are large because the buildout arrives before the full cash-flow payoff is known.

That creates two macro effects. First, it raises investment demand in parts of the economy that are already capacity constrained, especially power and construction. Second, it adds financing demand in capital markets. If the private sector's largest firms are borrowing more at the same time the sovereign is issuing more, the marginal buyer of duration becomes more important.

This is why the belly can remain heavy even when credit quality looks strong. The issue is not whether the largest technology firms can repay. The issue is whether the market can absorb the extra duration without demanding a higher yield. The answer may be yes at some price, but that price can be meaningfully higher than the old post-pandemic equilibrium.

Long End: Fiscal Risk and the Return of Term Premium

The long end of the curve is where fiscal arithmetic becomes unavoidable. A thirty-year Treasury bond is a promise that stretches across multiple business cycles, elections, inflation regimes, and debt-management strategies. Investors buying that bond need confidence not only in repayment but also in the real value of repayment.

For much of the post-pandemic period, long-end yields were influenced by large central-bank balance sheets, strong demand for safe assets, and confidence that inflation would eventually return to target. When the Federal Reserve reduces balance-sheet support relative to that period, the private sector must absorb more duration. At the same time, persistent fiscal deficits mean that Treasury supply remains large.

The term premium is the extra compensation investors demand for holding a long bond rather than rolling a sequence of short bonds. It can be thought of as:

`Long yield = expected average future short rates + term premium`

If expected short rates rise, long yields rise. But long yields can also rise because the term premium rises, even if the expected policy path is stable. That distinction is crucial. A term-premium shock is not simply a bet that the Fed will hike more. It is a repricing of the risk of owning duration in a world where issuance is large, inflation uncertainty is higher, and the marginal buyer is less price-insensitive than before.

Fiscal deficits are central to this repricing. Large deficits require large issuance. Large issuance requires buyers. If buyers believe fiscal policy lacks a credible consolidation path, they will ask for more yield. The market does not need to believe in default for this to matter. A higher inflation risk premium, a higher supply premium, or a higher uncertainty premium is enough.

Debt Sustainability Is a Pricing Problem Before It Is a Crisis

Markets often talk about debt sustainability as if it matters only during a crisis. That is too narrow. Debt sustainability can affect pricing long before any dramatic event. If investors become less comfortable with the path of debt relative to GDP, the Treasury curve can adjust through higher long-end yields, higher auction concessions, weaker demand at duration-heavy maturities, or steeper curves.

The basic fiscal arithmetic is:

`Debt ratio change depends on primary deficit + (interest rate - growth rate) x debt ratio`

When nominal growth is strong and interest rates are low, debt dynamics are easier. When interest rates rise and deficits remain large, the interest burden compounds. Higher yields increase government interest expense, which can require still more borrowing. That feedback loop does not need to become explosive to affect the curve. It only needs to make investors demand more compensation.

This is the Minsky-style balance-sheet point applied to the sovereign. Stability can create complacency when financing is cheap. But once financing costs rise, the same balance sheet becomes more fragile. The long end is the part of the curve that prices that fragility most directly.

Why the Curve Can Steepen Without a Growth Boom

A common mistake is to read a steeper curve as a simple growth signal. Sometimes that is right. If long yields rise because investors expect stronger growth and higher future short rates, a steepening curve can reflect optimism. But the curve in this framework can steepen for less benign reasons.

If the front end is pinned by high policy rates, the belly is pressured by duration supply, and the long end is pressured by fiscal term premium, the steepening is more about compensation than growth. Investors are not necessarily saying the economy is entering a powerful expansion. They may be saying that the compensation required to own duration has increased.

That difference matters for asset allocation. A growth-led steepening can support cyclicals, banks, and risk assets. A term-premium-led steepening can pressure valuation multiples, raise mortgage rates, increase corporate discount rates, and tighten financial conditions even if earnings remain healthy. The same curve shape can carry very different information depending on why it moved.

Valuation: Higher Yields Change the Discount Rate

Treasury yields are the base layer of valuation. When yields rise across the curve, the discount rate for nearly every asset class shifts. Equity multiples face pressure because future cash flows are discounted at a higher rate. Real estate faces pressure because cap rates and financing costs rise. Private credit and leveraged finance face pressure because refinancing becomes more expensive. Even high-quality corporate borrowers face a different hurdle rate.

The simplest valuation equation is:

`Value = expected cash flow / (discount rate - growth rate)`

If the discount rate rises and the growth rate does not rise by the same amount, value falls. This is why a term-premium move can matter even when the economy is not collapsing. It changes the rate at which investors capitalize future cash flows.

For AI-related companies, the irony is sharp. The same investment cycle that may support future productivity can also add to current duration supply and raise the cost of capital. If AI capex eventually lifts productivity, it can improve long-run growth and help absorb higher rates. But during the buildout phase, the financing demand arrives first. The payoff arrives later and remains uncertain.

The Investor's Map

The practical framework is to separate the curve into three questions.

First, is inflation falling fast enough to let the Fed cut? If not, the front end remains sticky. Second, can the market absorb Treasury issuance and corporate duration without higher yields? If not, the belly remains vulnerable. Third, is fiscal policy credible enough to keep term premium contained? If not, the long end remains under pressure.

These questions produce different trades and risks. A front-end rally requires confidence in disinflation and Fed easing. A belly rally requires relief from supply pressure or a strong wave of demand for intermediate duration. A long-end rally requires lower fiscal anxiety, lower inflation uncertainty, or renewed demand from price-insensitive buyers. Without those conditions, curve-wide upward pressure can persist.

Conclusion: One Curve, Three Macro Stories

The source thesis is that U.S. yields are under upward pressure across maturities, but not for a single reason. That is exactly the right way to read the chart. The front end is a higher-for-longer inflation story. The belly is a duration absorption story shaped by Treasury issuance and hyperscaler borrowing for AI infrastructure. The long end is a term-premium story driven by fiscal deficits, Treasury supply, less Federal Reserve balance-sheet support, and concern about long-run debt sustainability.

The result is a curve that looks simple but contains three separate regimes of risk. Inflation keeps short rates elevated. Supply makes intermediate maturities heavy. Fiscal uncertainty forces long-bond investors to demand more compensation. For portfolios, the implication is direct: the risk is not merely that rates are high. The risk is that every part of the curve now has its own reason to stay higher.

Comments