The Job-Switcher Premium Is Back, but This Is Normalization, Not Overheating

- Lingxiao Xu

- 18 hours ago

- 15 min read

The Return of the Job-Switcher Premium Is a Labor-Market Normalization Signal

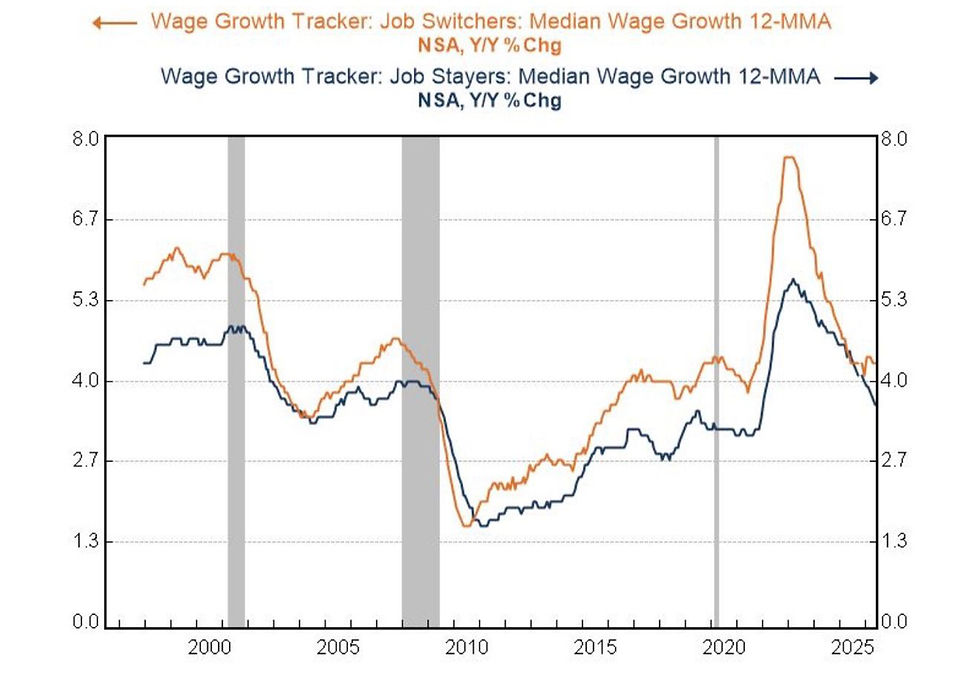

The latest wage-growth signal from the Atlanta Fed’s Wage Growth Tracker shows that the labor market’s traditional “switcher premium” has returned. Workers who change jobs are again receiving faster wage growth than workers who remain with their current employer. That may sound like a narrow labor-market detail, but it is an important macro signal. It tells us that the unusual inversion of 2024 and early 2025, when stayers temporarily enjoyed stronger wage growth than switchers, was not a new permanent structure. It was a cyclical artifact of a hiring slowdown, a sharp repricing of new-hire compensation, and the slower adjustment of incumbent pay.

Historically, job switchers have enjoyed a meaningful wage advantage. The reason is straightforward: a worker changing jobs usually enters an explicit market transaction. The outside employer must bid for the worker, and that bid reflects current labor demand, current vacancy pressure, and the worker’s bargaining power. A stayer, by contrast, is often governed by annual review cycles, internal compensation bands, promotion calendars, and retention budgets. The stayer’s wage is sticky. The switcher’s wage is marked closer to market.

That difference explains why the switcher premium is normally positive and why its recent inversion was so revealing. During the labor-market slowdown, wage growth for switchers fell faster than wage growth for stayers because new-hire compensation reacts almost immediately to weaker hiring demand. Employers can reduce signing offers, slow recruiting, widen candidate pools, and reset pay bands for new roles faster than they can cut or slow the pay of existing employees. Incumbent pay moves through institutional channels. New-hire pay moves through market channels.

The anomaly has now largely disappeared. Switcher wage growth has stabilized slightly above 4 percent, while stayer wage growth has continued drifting lower toward the mid-3 percent range. That restores the normal hierarchy: mobility is again being rewarded, but the reward is not explosively high. This is not the wage market of 2021 and early 2022, when scarce labor and frantic hiring created unusually large gains for movers. It is a cooler but more traditionally functioning labor market.

The investment question is what this normalization means. The answer is not a simple “labor market strong” or “labor market weak.” The more useful interpretation is that labor-market pricing is becoming less distorted. Hiring demand is no longer collapsing fast enough to punish switchers relative to stayers, but wage growth is also no longer broadening in a way that would signal an overheating labor market. That combination matters for Federal Reserve policy, service inflation, corporate margins, consumer income, and equity-market sector leadership.

Why the switcher premium normally exists

The switcher premium is a classic expression of labor-market search and matching theory. In the textbook model, workers and firms do not meet costlessly. Workers search for better matches, firms search for productive employees, and wages reflect bargaining over the surplus created by a match. When a worker changes jobs voluntarily, the move often occurs because the new match offers a higher expected surplus, a higher wage, better growth prospects, or some combination of the three.

Search models associated with Peter Diamond, Dale Mortensen, and Christopher Pissarides help explain why job mobility can produce wage gains. A worker who receives an outside offer has demonstrated that another firm values his labor more highly than the current wage implies. The outside offer also strengthens bargaining power. Even if the worker stays after counteroffer negotiations, the existence of the outside option matters. In a competitive labor market with frictions, mobility is one of the mechanisms through which workers discover and capture higher-value matches.

That is why job switchers usually receive larger wage increases than stayers. A stayer’s wage often adjusts through internal systems designed to preserve fairness, manage budgets, and avoid compression. Firms are reluctant to reprice every incumbent worker continuously because doing so is administratively costly and can create internal equity problems. A job switch, however, is a discrete pricing event. The new employer can offer a wage that reflects current external conditions without immediately repricing the entire existing workforce.

The traditional premium also reflects selection. Workers who switch jobs may have stronger outside options, more marketable skills, or a willingness to bear mobility costs. Employers bidding for them may be filling roles where demand is acute. The observed premium therefore combines pure market tightness with selection effects. Still, the direction of the premium is informative. When switchers are paid meaningfully more than stayers, external labor demand is strong enough to reward mobility. When the premium collapses or inverts, the market for new hires has weakened relative to the internal wage-setting process.

The recent return of the premium therefore says that outside labor-market pricing is no longer unusually depressed. It does not imply a return to excessive labor scarcity. It implies that market wages for movers have stopped deteriorating relative to sticky incumbent wages.

Why the inversion happened

The rare inversion of the switcher premium during much of 2024 and early 2025 was a textbook example of different wage-setting speeds. New-hire wages are fast-moving. Incumbent wages are slow-moving. When hiring demand slows abruptly, the first wage category to adjust is the wage offered to people being recruited today.

Companies can respond to weaker hiring demand by posting fewer roles, reducing signing bonuses, lowering offer ranges, delaying start dates, and becoming more selective. They can also fill roles internally rather than pay up for external talent. All of these choices reduce wage growth for switchers. The switcher wage is therefore a high-beta series with respect to hiring demand.

Stayer wages are different. Existing employees are protected by annual merit cycles, promotion paths, multi-year compensation norms, union contracts in some sectors, and retention concerns. Firms usually do not cut nominal wages for incumbents unless under severe stress. Even when wage growth slows, it often does so gradually. The compensation system creates inertia.

That inertia can cause a temporary inversion when the labor market cools. Suppose a company gave incumbents 5 percent increases during an inflationary period because it needed to retain staff and offset cost-of-living pressure. Then hiring demand slows. New offers that previously would have included 7 percent or 8 percent increases over a worker’s prior wage are reset to 3 percent or 4 percent. For a period, stayers can look better than switchers, even though that is not the normal hierarchy. The difference is not because staying suddenly became more valuable as a structural economic fact. It is because incumbent wages adjust with a lag.

This is exactly why the inversion was useful. It marked a point at which the marginal price of labor had cooled faster than the average wage paid to existing workers. That is the same distinction inflation analysts often make between marginal rents and average rents. New-lease rents adjust quickly to market conditions; the rent paid by the average tenant adjusts slowly as leases roll. New-hire wages are the labor-market equivalent of new-lease rents. Incumbent wages are closer to average rents.

The disappearance of the inversion means the fast-moving and slow-moving wage series are no longer sending such contradictory messages. New-hire wage growth has stabilized, while incumbent wage growth is still decelerating. The labor market is not snapping back to boom conditions. It is converging toward a more internally consistent equilibrium.

What the current readings imply

The current configuration matters because both sides of the spread are informative. Switcher wage growth slightly above 4 percent is not weak in absolute terms. It suggests that workers who move still have bargaining power and that employers still need to pay for outside talent. But it is also far below the extremes of the post-pandemic labor shortage. The fever has broken.

Stayer wage growth drifting toward the mid-3 percent range is also important. It suggests that the slower-moving incumbent wage process continues to cool. That is helpful for the disinflation story, especially in labor-intensive services. If stayer wage growth had remained elevated while switcher wage growth reaccelerated, the Fed would have a more serious wage-pressure problem. Instead, the current pattern points to a labor market that is normalizing rather than reigniting.

The spread between switchers and stayers can be thought of as a mobility premium:

Mobility premium = wage growth for job switchers - wage growth for job stayers.

When the premium is positive but modest, workers are rewarded for taking external opportunities, but employers are not engaged in a panic bidding war. When the premium is negative, outside hiring demand is weak enough to make mobility less rewarding than staying. When the premium is extremely positive, labor demand is tight enough to create wage-driven inflation risk and margin pressure. Today’s signal is closer to the first case: normal, positive, and contained.

This has three macro implications. First, the labor market is not collapsing. A collapsing market would likely keep switcher wage growth under pressure and might produce renewed weakness in mobility. Second, the labor market is not overheating. A wage-price spiral story would require broader acceleration, not merely a modest positive switcher premium. Third, the labor market is becoming cleaner to interpret. The rare inversion distorted the usual signal; its disappearance restores the historical relationship between mobility and wage gains.

For investors, that third point is valuable. Markets often struggle when labor data send contradictory messages. Payroll growth, unemployment claims, quits, job openings, average hourly earnings, and wage trackers can all point in slightly different directions. The switcher-stayer normalization reduces one contradiction. It says the wage market is no longer in an abnormal state where sticky incumbent pay is masking a much weaker external hiring market.

Implications for inflation and the Federal Reserve

The Federal Reserve cares about wage growth because labor is the dominant cost in many service industries. Wage growth does not mechanically determine inflation, but it affects unit labor costs, margins, and the pricing behavior of firms. If nominal wage growth runs persistently above productivity growth plus the inflation target, firms must either absorb margin compression or raise prices.

A simple framework is:

Sustainable wage growth ≈ productivity growth + inflation target.

If trend productivity is around 1.5 percent and the inflation target is 2 percent, sustainable wage growth might be around 3.5 percent. If productivity is stronger, the economy can sustain higher wage growth without inflation pressure. If productivity is weaker, even moderate wage growth can pressure margins and prices. Current stayer wage growth drifting into the mid-3 percent range is therefore broadly consistent with a more benign inflation backdrop, especially if productivity growth remains firm. Switcher wage growth slightly above 4 percent is less benign, but because it applies to movers rather than the entire workforce, it is not by itself a disinflation breaker.

The Fed’s reaction function depends on whether wage pressure is broadening or narrowing. A renewed surge in switcher wages combined with rising quits, accelerating payrolls, and higher services inflation would be hawkish. A modest restoration of the switcher premium while stayer wages continue to cool is different. It tells policymakers that labor-market function is improving without obvious reacceleration in aggregate wage pressure.

This distinction matters for rates. If the Fed reads the wage data as normalization, not overheating, the return of the premium should not force a hawkish repricing. It may even support a soft-landing interpretation: workers still have enough mobility to sustain income growth, firms are not cutting aggressively, but wage growth is cooling enough to be compatible with lower inflation over time.

However, the Fed cannot ignore the level of wages entirely. Services inflation is sticky, and wage growth above 4 percent for switchers can still matter if it spreads. The key is whether the switcher premium remains modest or starts widening rapidly. A stable premium around current levels is consistent with normalization. A sharp widening would suggest renewed competition for labor and could challenge the disinflation narrative.

Corporate margins and sector effects

For companies, the return of the switcher premium has mixed implications. On the one hand, a positive premium means external hiring is no longer cheap relative to incumbent labor. Firms that need specialized talent may have to pay up again, especially in sectors where skills remain scarce. That can pressure margins for labor-intensive industries.

On the other hand, the premium is modest and stayer wage growth is cooling. That combination is less threatening than a broad wage acceleration. Companies may face selective talent costs without facing a generalized wage shock. For many firms, the more important margin variable is the pace of incumbent wage growth, because incumbents are the larger share of total payroll. If stayer wage growth continues moving toward the mid-3 percent range, aggregate labor-cost pressure should ease.

The sector implications vary. Labor-intensive services such as restaurants, hospitality, healthcare services, logistics, and retail are most sensitive to wage trends. A modest positive switcher premium can raise hiring costs, but cooling stayer wages may help stabilize total labor expense. Companies with high turnover are more exposed to switcher wage dynamics because they continually reprice labor through new hires. Companies with low turnover are more exposed to stayer wage cycles.

Technology and professional services require a more nuanced reading. In some white-collar sectors, hiring demand slowed sharply after the pandemic boom. The return of a switcher premium may indicate that the worst of the new-hire wage reset has passed, but it does not necessarily imply a broad hiring boom. It may simply mean that compensation for scarce roles has stabilized while lower-demand roles remain soft.

For margins, the most useful question is whether revenue growth can outrun labor-cost growth. If nominal revenue growth is healthy and wage growth is cooling, margins can improve. If revenue growth slows while wages remain sticky, margins compress. The switcher-stayer configuration suggests less wage pressure than the post-pandemic peak but more labor resilience than a recessionary downturn. That is generally supportive of a soft-landing earnings environment.

Consumer income and spending

The return of the switcher premium also matters for household income. Job switching is one channel through which workers raise lifetime earnings. When mobility pays, households have a stronger incentive to search, move, and improve matches. That can support aggregate income growth and consumer confidence, especially among workers with marketable skills.

But the current premium is not large enough to imply a new consumer boom. Switchers are doing better than stayers, but wage growth for both groups has moderated from prior extremes. The signal is therefore consistent with resilient but cooling consumption. Workers still have income support, but the impulse is not accelerating in a way that would necessarily restart high inflation.

This is important for equity markets. Consumer-facing companies need enough wage growth to support demand but not so much that labor costs destroy margins. The current wage setup is closer to that balance than the extremes of 2021–2022. It supports spending without clearly indicating a wage spiral.

There is also a distributional angle. Job-switching gains accrue mostly to workers who can move, have bargaining power, and face demand for their skills. Workers with fewer outside options may not benefit as much. Stayer wage growth cooling into the mid-3 percent range may feel less generous in categories where household costs remain elevated. The macro aggregate may look balanced, while household experiences diverge.

Investors should therefore avoid treating the switcher premium as a simple consumer signal. It is better viewed as one component of labor income. It should be read alongside employment growth, hours worked, real wage growth, delinquency data, and spending patterns. Its message is constructive but not euphoric.

Portfolio interpretation

The return of the switcher premium supports a soft-landing interpretation more than a recession or overheating interpretation. It indicates that the labor market is functioning more normally, that external wage offers have stabilized, and that incumbent wage growth is gradually cooling. For asset allocation, that mix is generally friendly to risk assets, but it is not an unqualified green light.

For bonds, the signal is modestly supportive if investors interpret it as wage normalization. Cooling stayer wages are consistent with lower services inflation over time. A modest switcher premium should not, by itself, force the Fed to tighten further. The bond risk is that switcher wage growth keeps rising and begins pulling aggregate wage measures higher. That would be a different signal.

For equities, the setup favors companies that benefit from resilient income and lower wage pressure. Broad consumer demand can remain supported, while labor-cost inflation becomes less severe. This is constructive for quality consumer services, select retailers with pricing discipline, and firms with operating leverage to stable demand. It is less favorable for companies that depend on cheap hiring or very high turnover, because new-hire costs are no longer falling relative to incumbent pay.

For style factors, the signal is balanced. It is not recessionary enough to demand a pure defensive posture. It is not inflationary enough to demand a pure commodity or rate-hedge posture. It is more consistent with quality cyclicals, steady-margin compounders, and selective labor-sensitive names where wage pressure has already been priced in.

The key risk is overinterpretation. A restored switcher premium is not the same thing as a booming labor market. It is a return to hierarchy after an unusual inversion. Investors should use it as confirmation that the labor market is normalizing, not as proof that hiring demand is accelerating aggressively.

A compact regime map

The switcher-stayer spread is most useful when it is placed in a broader labor-market regime map. A positive switcher premium can mean different things depending on whether aggregate wage growth is rising or falling, whether unemployment is stable or increasing, and whether companies are still expanding headcount. The same spread can be benign in one regime and inflationary in another.

One useful framework has four quadrants. In the first quadrant, switcher wages are rising faster than stayer wages, and both series are accelerating. That is the overheating quadrant. Mobility pays, incumbent pay is also catching up, and labor-cost pressure is likely broad enough to worry the Fed. This was closer to the 2021–2022 environment, when quits were elevated, job openings were plentiful, and employers were forced to bid aggressively for workers.

In the second quadrant, switcher wages rise faster than stayer wages, but both series are stable or decelerating. That is the normalization quadrant. Mobility pays again, but wage pressure is not broadening. The current data look closer to this regime. The external market is no longer unusually weak, but the overall wage impulse is cooling.

In the third quadrant, switcher wages fall below stayer wages while both series decelerate. That is the slowdown quadrant. New-hire pricing has weakened, incumbent pay is gradually catching down, and firms are likely more cautious about hiring. The 2024 and early-2025 inversion fit this description. It was not immediately recessionary, but it was a sign that marginal labor demand had softened materially.

In the fourth quadrant, switcher wages fall below stayer wages while stayer wages remain high. That is the uncomfortable margin-squeeze quadrant. Firms are not bidding for new labor, but they are still carrying a sticky incumbent wage bill. That combination can hurt margins if revenue growth is slowing. It can also delay disinflation because average labor costs remain elevated even as new hiring weakens.

This regime map helps avoid the biggest mistake in interpreting the latest chart: treating the sign of the spread as sufficient. The sign matters, but the level and direction of both components matter more. A positive spread with switchers at 4.1 percent and stayers at 3.6 percent is very different from a positive spread with switchers at 7 percent and stayers at 5.5 percent. Both are positive. Only one screams overheating.

Today’s signal is therefore constructive precisely because it is moderate. The historical hierarchy has returned, but the level of wage growth is not back at the most inflationary phase of the cycle. That is why the data lean toward normalization rather than renewed labor-market excess.

How the signal could fail

The first failure mode is renewed acceleration. If switcher wage growth pushes decisively higher from slightly above 4 percent toward the 5 percent or 6 percent range, while stayer wage growth stops falling, the benign interpretation weakens. That would indicate that external labor demand is again forcing employers to pay up and that incumbent compensation may follow with a lag. In that scenario, the switcher premium would become a leading inflation-risk signal rather than a normalization signal.

The second failure mode is a false stabilization. Switcher wages may be stabilizing now because the fastest adjustment is over, not because hiring demand has truly improved. If job openings resume falling, unemployment rises, and quits weaken, switcher wage growth could roll over again. The premium might remain positive for a while if stayer wages fall faster, but the macro message would become less constructive. A positive spread is not enough if both series are falling for recessionary reasons.

The third failure mode is sector concentration. Aggregate switcher wages can look stable even if strength is concentrated in a few high-skill categories while broad labor demand remains weak. In that case, the signal would be less useful for the whole economy. Investors should therefore compare the aggregate tracker with sector-level hiring data, small-business hiring plans, temporary-help employment, and professional-services demand.

The fourth failure mode is productivity disappointment. Wage growth that looks sustainable under a 1.5 percent or 2 percent productivity assumption can become inflationary if productivity slows. The wage-inflation relationship is not just about nominal wages; it is about wages relative to output per hour. If productivity weakens while wage growth remains near 4 percent, unit labor costs can reaccelerate even if the switcher premium itself looks moderate.

The fifth failure mode is policy interpretation. Markets may initially read the premium’s return as soft-landing evidence, but the Fed may emphasize that wage growth remains above levels fully consistent with 2 percent inflation. If inflation data are sticky at the same time, policymakers may not give the labor-market normalization signal much credit. The wage signal does not operate in isolation; it is filtered through inflation prints, financial conditions, and the Fed’s risk-management preferences.

These risks do not overturn the base case. They define the monitoring framework. The switcher premium is useful because it changes early when hiring demand changes. But like all early indicators, it must be confirmed by a broader dashboard before it becomes a high-conviction macro conclusion.

What to watch next

The next confirmation should come from mobility and hiring data. If the switcher premium remains positive while quits stabilize and job openings stop deteriorating, the normalization story strengthens. If the premium widens sharply alongside rising quits and accelerating employment cost data, inflation risk increases. If the premium turns negative again, the labor-market slowdown may be reasserting itself.

Average hourly earnings and the Employment Cost Index will also matter. The Atlanta Fed tracker is useful because it tracks the same individuals over time and separates switchers from stayers, but policymakers and markets will cross-check it against broader compensation measures. The most benign outcome would be stable switcher wage growth, continued cooling in stayer wage growth, and moderate aggregate compensation growth.

Services inflation is the final test. Wage data matter because they can feed service prices. If service inflation continues cooling while the switcher premium remains modestly positive, the Fed can view the premium as normal labor-market function. If service inflation stalls or reaccelerates, the same wage data will be interpreted more cautiously.

For now, the signal is clear. The rare inversion has ended. Job mobility is again being rewarded. But the reward is moderate, not excessive. The labor market looks less distorted, not newly overheated.

Conclusion: normal does not mean hot

The restoration of the switcher premium is a useful macro signal because it resolves an unusual contradiction in the wage data. During the slowdown, new-hire compensation adjusted quickly to weaker demand, while incumbent wages moved slowly through annual reviews and internal pay structures. That caused stayers to temporarily outpace switchers, a rare outcome in the Atlanta Fed’s 25-year history.

Now the traditional hierarchy has returned. Switcher wage growth has stabilized slightly above 4 percent, while stayer wage growth continues to ease toward the mid-3 percent range. That points to a labor market that is neither collapsing nor overheating. It is becoming more normal.

For markets, this is a soft-landing signal with conditions. It supports the idea that labor income remains resilient enough to sustain consumption, while wage pressure is cooling enough to keep disinflation alive. The Fed can tolerate a modest switcher premium if it does not broaden into aggregate wage acceleration. Equity investors can welcome normalization, but they should watch whether the premium stays contained.

The key message is simple: mobility pays again, but not wildly. That is what a healthier, cooler labor market should look like.

Comments